vol. 02 · tier 02 // ch. 03 of 10 · intermediate course

Options Basics

An option is the right (not obligation) to buy or sell an asset at a fixed price by a fixed date. You pay a premium for this right.

- read

- ~4 min

- length

- 1,334 words

- position

- 03 of 10

3. Options Basics

An option is the right (not obligation) to buy or sell an asset at a fixed price by a fixed date. You pay a premium for this right.

Most retail option traders lose money because they treat options like lottery tickets. We won’t.

Two types

| Option | Right to | Used by buyer when bullish/bearish? |

|---|---|---|

| Call (CE) | Buy the underlying | Bullish |

| Put (PE) | Sell the underlying | Bearish |

Anatomy of an option

- Strike price (K) — the price at which you have the right to transact.

- Expiry — when the right vanishes.

- Premium — what you pay/receive.

- Lot size — same as futures.

- Style — Indian index/stock options are European (exercise only at expiry).

Example

Nifty 24500 CE June expiry @ ₹150 premium

- Right to “buy” Nifty at 24,500.

- Premium ₹150 × lot 25 = ₹3,750 paid.

- At expiry, if Nifty = 24,800: intrinsic value = 300, profit = 300 − 150 = ₹150/share = ₹3,750.

- If Nifty ≤ 24,500 at expiry: option expires worthless. You lose the entire ₹3,750.

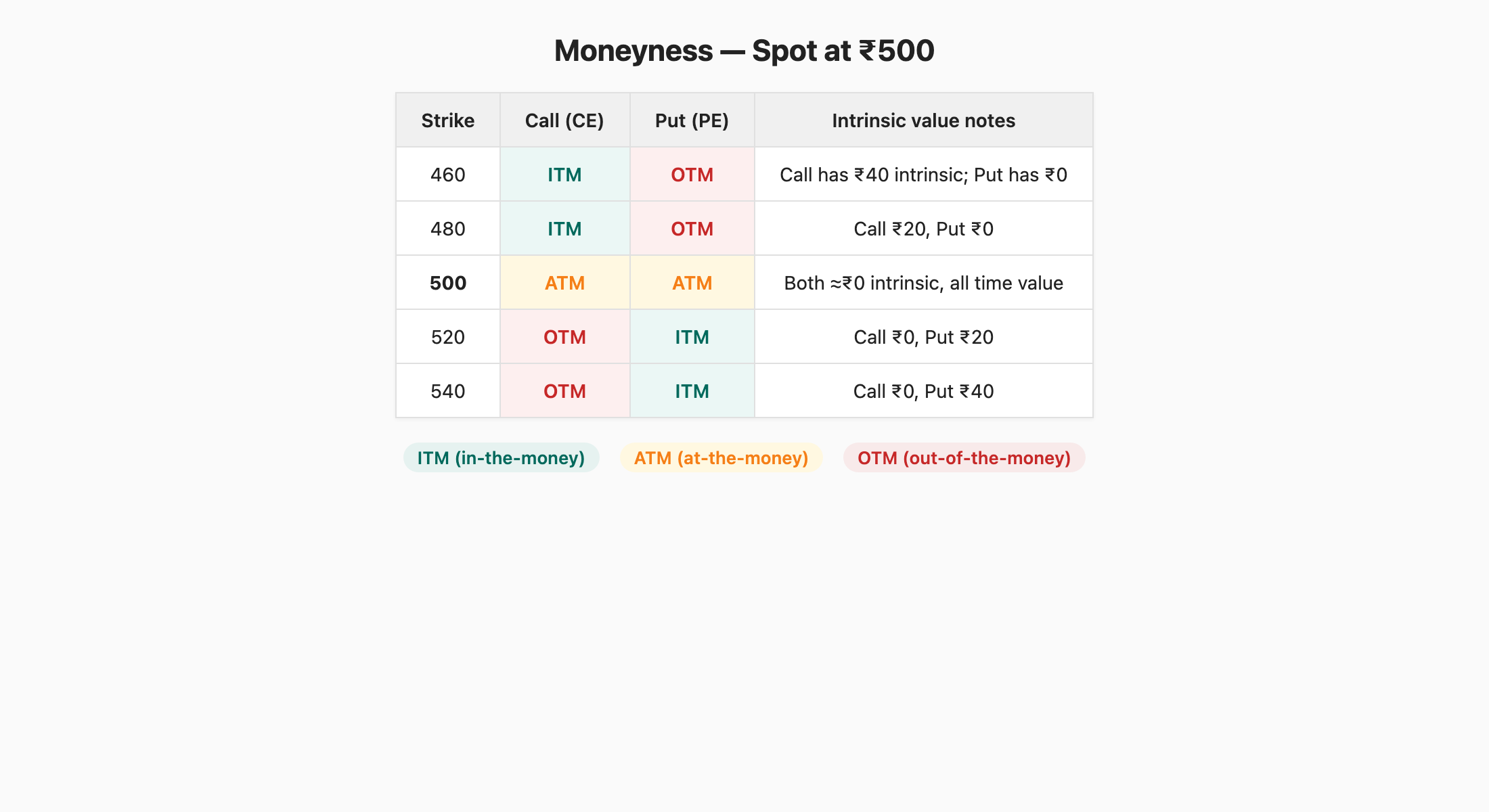

Moneyness

| For a Call | For a Put | Term |

|---|---|---|

| Spot > Strike | Spot < Strike | ITM (In-The-Money) — has intrinsic value |

| Spot ≈ Strike | Spot ≈ Strike | ATM (At-The-Money) |

| Spot < Strike | Spot > Strike | OTM (Out-of-The-Money) — only time value |

With spot at ₹500, scan the table top-to-bottom. The green ITM cells mark strikes where the option already has real value baked in: a 460 Call lets you “buy at ₹460” when the market price is ₹500 — that’s a guaranteed ₹40 of intrinsic value, plus whatever extra time value the market layers on top. Mirror image for puts on the bottom rows. The amber ATM row at strike 500 is the indecision zone — both call and put have zero intrinsic value, so the entire premium is time value (the market betting on which way it’ll move). The red OTM cells are pure lottery tickets — strikes too far away to be worth anything intrinsically yet, just hope and time decay.

When you read an option chain, this picture is what you’re navigating: ITM = expensive but high probability, ATM = balanced, OTM = cheap but most likely to expire worthless.

Intrinsic vs Time value

- Intrinsic = how deep ITM (max(0, S−K) for calls, max(0, K−S) for puts).

- Time value = the rest. Decays as expiry nears (theta decay).

Why OTM options “feel cheap” but are usually losing trades

A 24,800 CE when Nifty is at 24,500 might cost just ₹40. But for it to be profitable, Nifty must rally 1.4% AND that move must happen before time value erodes. Probability < 30%. Most expire worthless.

Buying vs selling options

| Buyer | Seller (writer) | |

|---|---|---|

| Pays | Premium | Receives premium |

| Risk | Limited to premium | Potentially unlimited (calls) |

| Reward | Unlimited (theoretically) | Limited to premium |

| Margin | Just the premium | Full SPAN + Exposure |

| Time decay | Hurts you | Helps you |

| Win rate | Low (~30–35%) | High (~65–75%) |

Reality check: ~80–90% of option buyers lose money over a year. Sellers win more often, but blow-ups are catastrophic.

Payoff diagrams

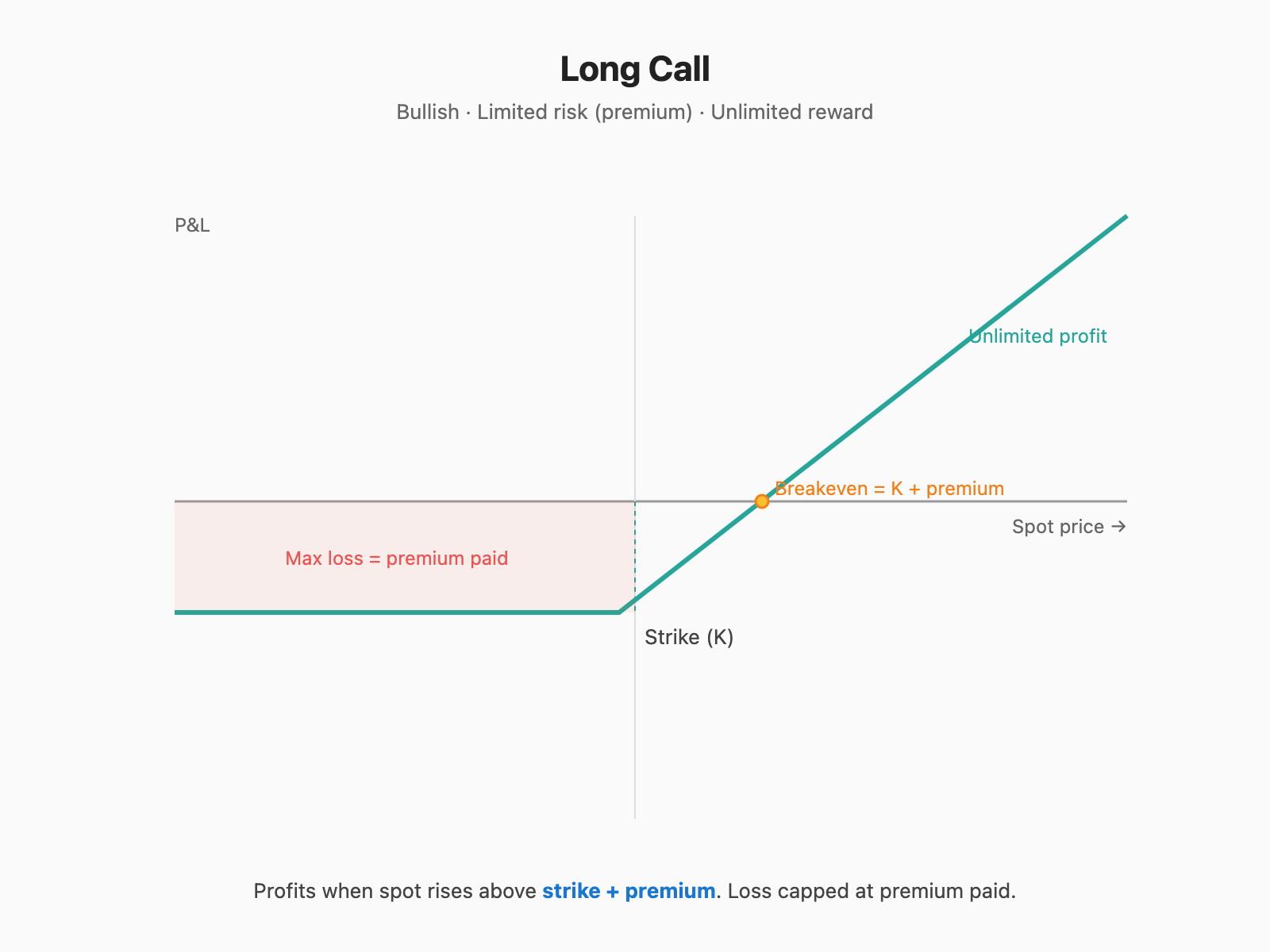

Long Call

Read the line left to right. While spot is below the strike (left half), the line sits flat at a small loss — you’ve paid the premium and the option is worthless on expiry. The line stays flat right up to strike. Past the strike, it ticks down to crossing zero at K + premium (the yellow breakeven dot) and then climbs unboundedly. Max loss = premium paid; max profit = unlimited. That’s the entire promise of a long call in one picture.

Read the line left to right. While spot is below the strike (left half), the line sits flat at a small loss — you’ve paid the premium and the option is worthless on expiry. The line stays flat right up to strike. Past the strike, it ticks down to crossing zero at K + premium (the yellow breakeven dot) and then climbs unboundedly. Max loss = premium paid; max profit = unlimited. That’s the entire promise of a long call in one picture.

- Breakeven: K + premium.

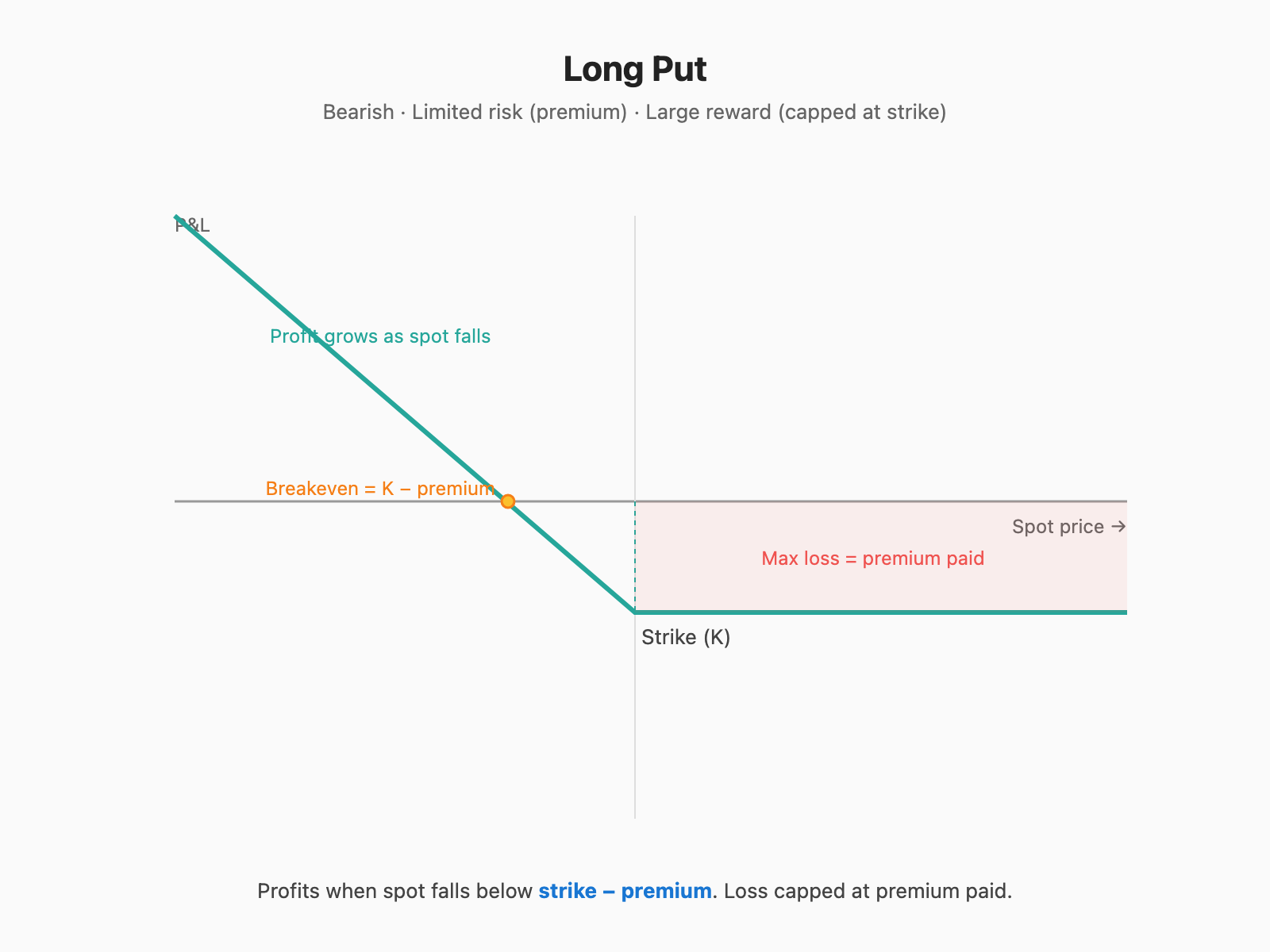

Long Put

Mirror image. The flat-loss zone is now on the right (spot above strike, put expires worthless), and profit grows as spot falls below K − premium. Profit is large but not technically infinite — it’s capped by the stock going to zero. Same trade structure as a call, just the bearish version.

Mirror image. The flat-loss zone is now on the right (spot above strike, put expires worthless), and profit grows as spot falls below K − premium. Profit is large but not technically infinite — it’s capped by the stock going to zero. Same trade structure as a call, just the bearish version.

- Breakeven: K − premium.

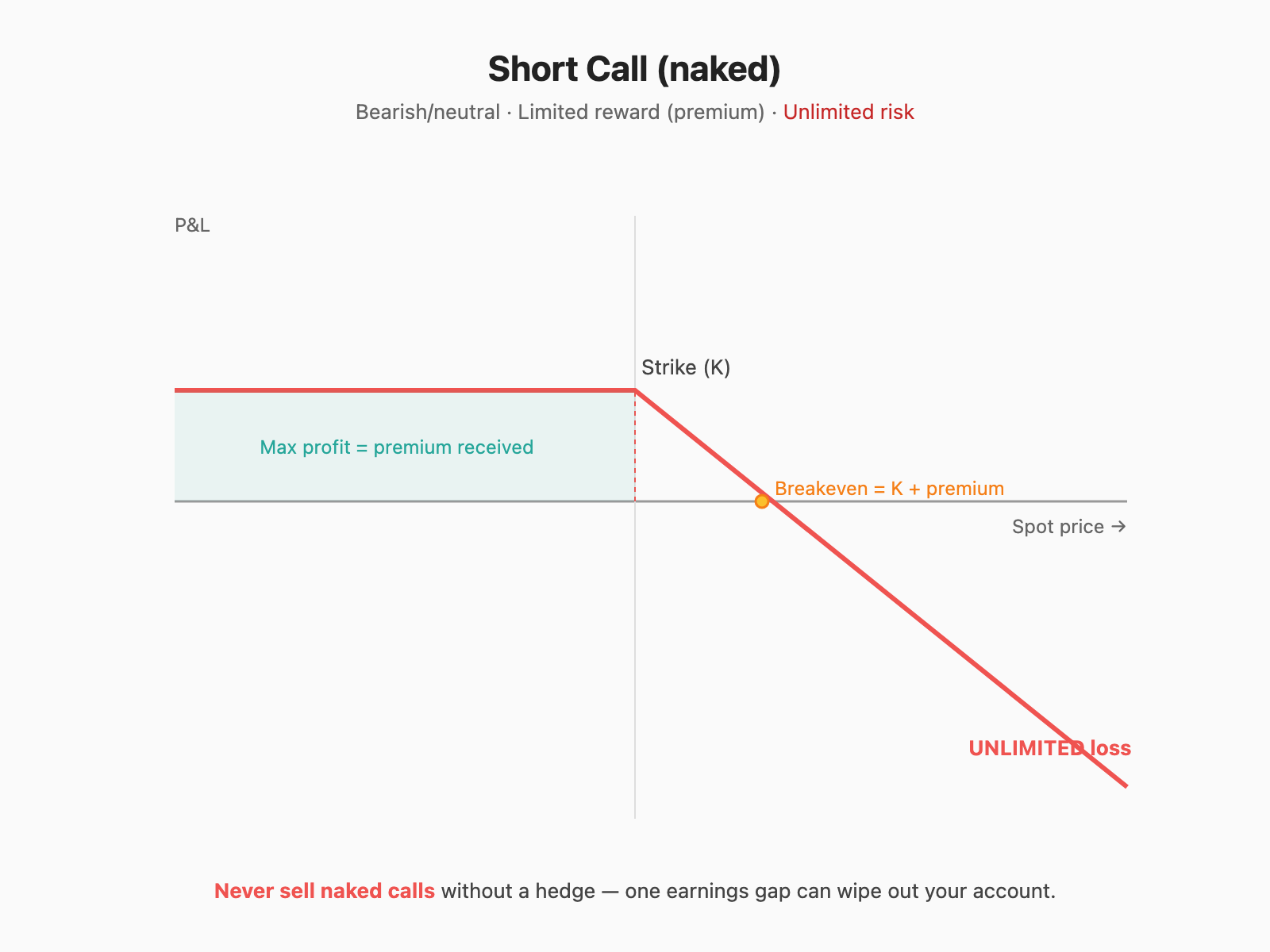

Short Call (very risky, unlimited loss)

Now flip the long call upside down. While spot stays below strike, you keep the entire premium (the flat green region on the left). But the moment spot pushes past K + premium, the line dives — and never stops diving. There’s no theoretical ceiling on a stock’s price, so there’s no ceiling on this loss. This is the picture every “easy income from selling options” pitch conveniently hides.

Now flip the long call upside down. While spot stays below strike, you keep the entire premium (the flat green region on the left). But the moment spot pushes past K + premium, the line dives — and never stops diving. There’s no theoretical ceiling on a stock’s price, so there’s no ceiling on this loss. This is the picture every “easy income from selling options” pitch conveniently hides.

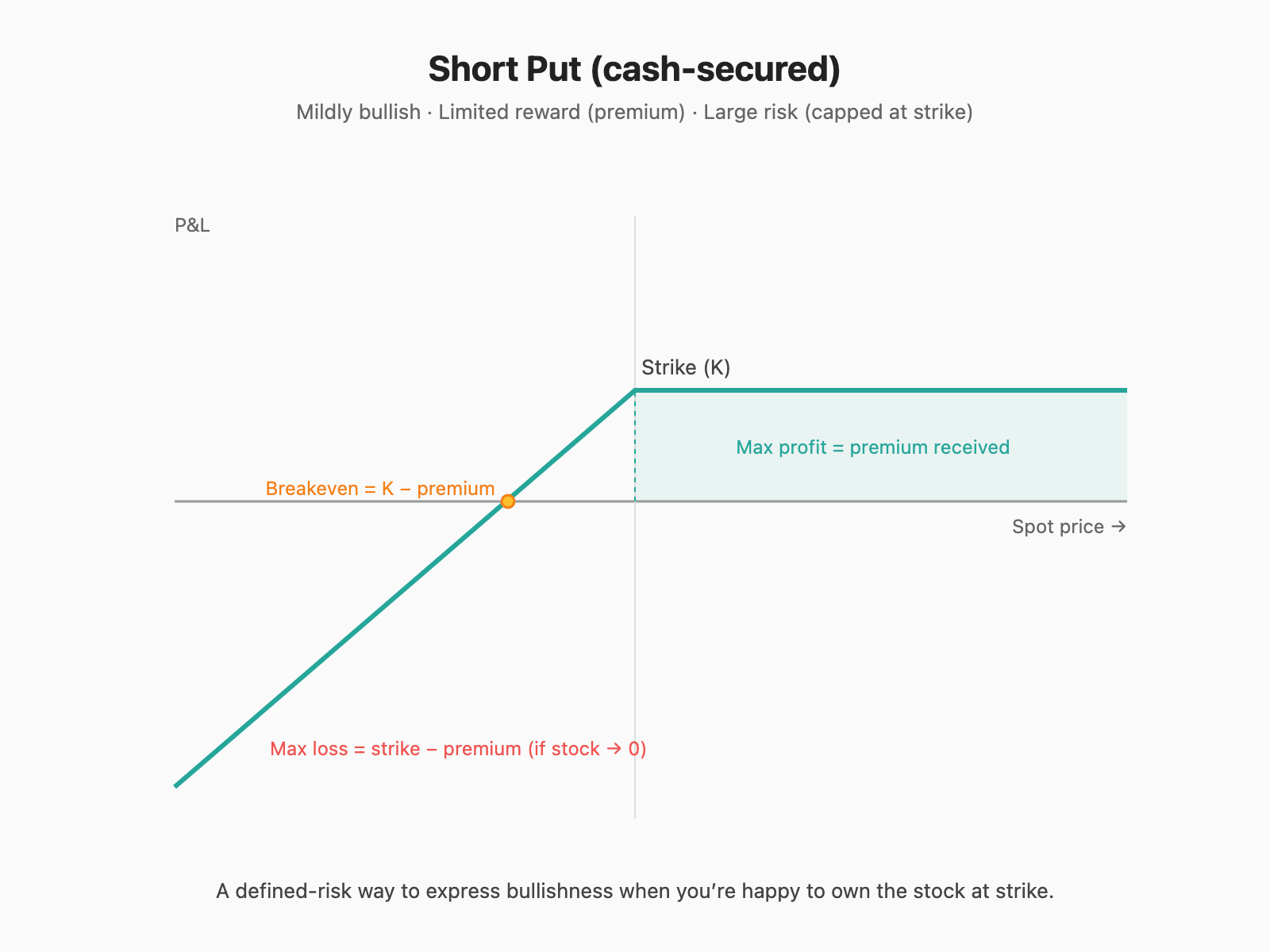

Short Put (cash-secured)

Mirror of the short call — flip the long put upside down. Profit capped at premium received (right side, flat green), loss grows as spot falls below K − premium, and the worst case is the stock going to zero (so loss is large but bounded, unlike the short call). This is why short puts are considered much safer than short calls: there’s a worst case you can plan for. “Cash-secured” means you’ve parked enough cash to actually buy the stock at strike if assigned — a way to express bullishness while collecting premium.

Mirror of the short call — flip the long put upside down. Profit capped at premium received (right side, flat green), loss grows as spot falls below K − premium, and the worst case is the stock going to zero (so loss is large but bounded, unlike the short call). This is why short puts are considered much safer than short calls: there’s a worst case you can plan for. “Cash-secured” means you’ve parked enough cash to actually buy the stock at strike if assigned — a way to express bullishness while collecting premium.

Max loss = strike − premium (if stock goes to 0).

Option chain — how to read it

Across a single expiry, every available strike is listed:

| Calls (LTP, OI, IV) | Strike | Puts (LTP, OI, IV) |

|---|---|---|

| 380 | 24300 | 30 |

| 250 | 24400 | 50 |

| 150 | 24500 (ATM) | 140 |

| 80 | 24600 | 250 |

| 35 | 24700 | 380 |

What to look for:

- Highest OI on call side = market sees that strike as resistance.

- Highest OI on put side = strike seen as support.

- OI buildup changes intraday show where smart money is positioning.

- PCR (Put-Call Ratio) = total put OI / total call OI. > 1 typically bullish (more puts = hedging), < 0.7 bearish (complacency).

Implied Volatility (IV)

The market’s expectation of future volatility, baked into the premium.

- High IV → expensive options. Good for selling, bad for buying.

- Low IV → cheap options. Good for buying.

- IV crush — IV drops sharply after a known event (earnings, RBI policy) → premiums collapse even if direction was right.

A common rookie disaster: buying a call before earnings on a “sure” stock. Stock pops 3% next morning, but IV crashes from 60 to 35 → premium drops despite the move. You were directionally right and still lost money.

Beginner-safe option strategies

| Strategy | View | Risk | Reward |

|---|---|---|---|

| Long Call / Long Put | Strong directional | Premium | Unlimited |

| Bull Call Spread | Mildly bullish | Limited | Limited |

| Bear Put Spread | Mildly bearish | Limited | Limited |

| Cash-secured Put | Mildly bullish + ok to own stock | Strike − premium | Premium |

| Covered Call | Own stock, expect sideways | Stock downside | Premium |

Avoid as a beginner: Naked short options, straddles/strangles, short iron condors. They look easy until vol spikes and your account vaporizes.